Inventory Expansion and Market Rebalancing

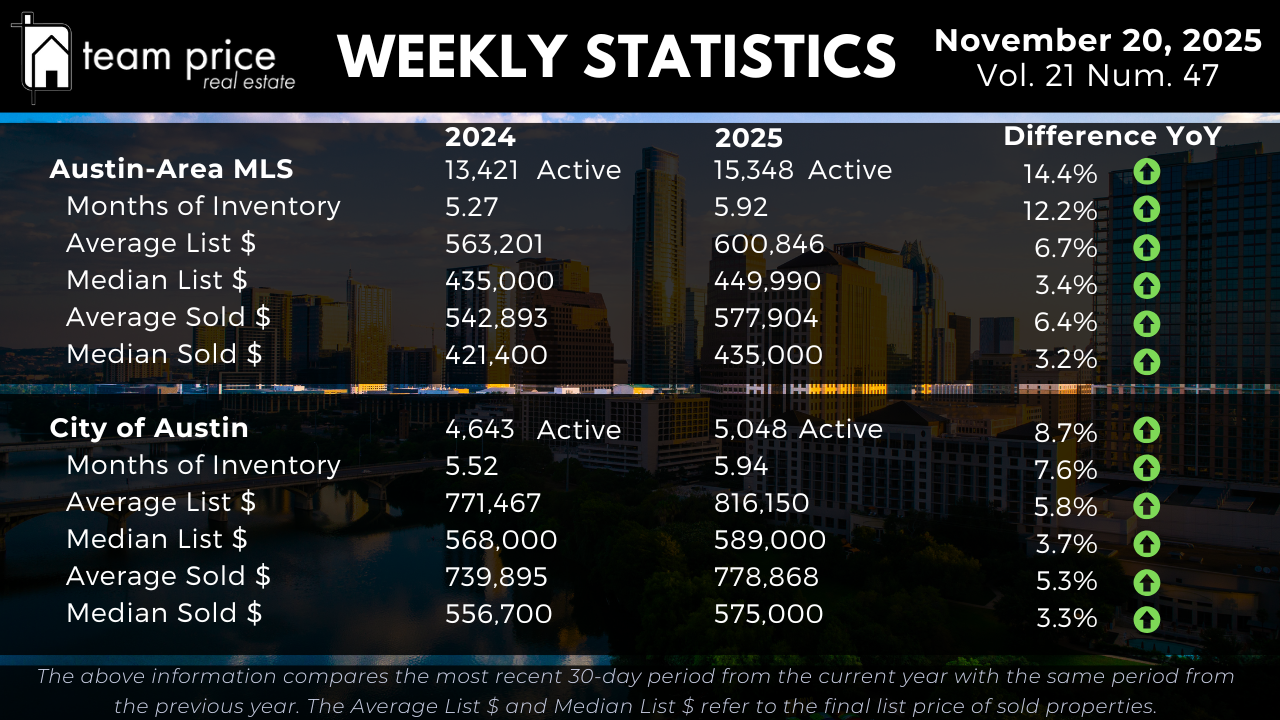

The Austin housing market continues to move further into supply-led conditions as inventory grows faster than demand absorbs it. Active listings across the Austin-Area MLS are up 14.4% year over year, rising from 13,421 to 15,348. Based on current absorption rates, Months of Inventory has increased from 5.27 to 5.92 — a 12.2% rise, or roughly a 1.1× increase in available supply compared with last year. This confirms longer marketing times and an expansion of buyer choice as the fourth quarter progresses.

Within the City of Austin, inventory growth is more moderate but still notable. Active listings increased 8.7%, from 4,643 to 5,048, while Months of Inventory climbed from 5.52 to 5.94, a 7.6% increase. The city is tracking in line with the metro-level supply expansion pattern, indicating a continued shift toward a balanced-to-softening environment.

Rather than a short-term fluctuation, the rise in supply remains part of a broader normalization process. Buyers now benefit from meaningful selection and additional leverage, while sellers must adjust through accurate pricing, competitive presentation, and disciplined timing.

Pricing Trends and Market Direction

Price levels remain stable with modest growth. Across the Austin-Area MLS, the average active list price increased 6.7% year over year, moving from $563,201 to $600,846. Median active list price rose 3.4%, from $435,000 to $449,990. Similar to previous months, pricing gains are more concentrated at the upper end, while median movement demonstrates broader market stability rather than acceleration.

Recent closing data reflects the same pattern. The average sold price increased 6.4% year over year to $577,904, while the median climbed 3.2% to $435,000. Within the City of Austin, the average sold price increased 5.3%, from $739,895 to $778,868. The median sold price improved from $556,700 to $575,000, a 3.3% rise year over year. These median-level increases indicate pricing equilibrium, where market participants are aligned and aggressive upward pressure remains contained.

Directionally, the price structure is holding steady. Sellers continue testing elevated list prices, but buyers remain highly value-aware. This is still a negotiation-first market defined by discipline rather than urgency.

Negotiation Environment and Buyer Leverage

Negotiation conditions continue to favor buyers. So far this month, 70.38% of all sold properties have closed below the list price (compared with 70.89% last month), while 18.86% closed at list and 10.76% above it. The slight uptick in over-ask closings reflects targeted competition where inventory is tight and listings are strategically positioned.

The average sold-to-list price ratio now stands at 97.08%, confirming sellers are conceding roughly 2.9% on average. This mirrors recent trendlines and reinforces that while concessions are standard, they have stabilized. Sellers who price accurately and present well still secure efficient outcomes; those who overshoot are encountering longer days on market and deeper adjustments.

Precision is now the operational advantage. Buyers hold leverage through wider selection and a slower pace of bidding, while sellers win when their pricing aligns with market reality.

Regional & ZIP Code Performance

Market behavior across Central Texas is balanced and data-driven. Month over month, 21 out of 30 tracked cities (70%) posted price increases, while 9 (30%) declined. Year over year, 16 cities (53%) have gained, and 14 (47%) have declined.

Among 75 ZIP codes, 39 (52%) show month-over-month price gains, while 36 (48%) are down. On a year-over-year basis, 38 ZIP codes (51%) are up and 36 (48%) are down. Only one ZIP code remains above its 12-month peak, while 74 are below, confirming widespread normalization and the conclusion of the corrective cycle.

Location-specific performance — particularly around affordability and school district alignment — now drives most variance, not broad-based market shifts.

Prices Relative to Peak Levels

Relative to recent peaks, the market remains well off surge-era highs but has clearly established stability. In the Austin-Area MLS: Average sold price is 13.2% below its May 2022 peak. Median sold price is down 19.1% from peak. Price per square foot remains roughly 20–22% below peak values, holding consistent with correction-level metrics seen in recent months.

Within the City of Austin: Median sold price is 15.4% below its May 2022 high. Average sold price is down 13.1% from peak. Price per square foot has declined between 22–26%, depending on average vs median. These declines are structural, not temporary. The market completed its downward reset long ago and is now operating in a steady post-correction environment.

Market Outlook

As of late 2025, the Austin housing market is stabilizing following a high-volume correction phase. Supply continues to grow at double-digit rates, yet pricing remains intact, and calibrated listings still find demand. Over-ask activity is rising incrementally but remains limited to micro-market pockets of scarcity and strong product alignment.

The path forward is clear: Buyers maintain control of timing and negotiation. Sellers succeed through accuracy, not optimism. Pricing is governed by value justification, not momentum. The market has transitioned out of volatility and into structured balance, building the foundation for a more predictable cycle as we move into 2026.